Power of Indexing

Potential can be such an enticing, positive word. Potential can also be a negative word. Potential checks don’t cash very well at the bank. Potential returns are marketed to consumers, and consumers invest for potential all the time. Potential returns, at some point, are not really useful to you.

If I could guarantee you an average rate of return of +20% over the next two years, would you take it?

- If you invest $100,000 and have a 100% gain in the first year, at the end of the year balance is $200,000.

- In year two, let’s say your investment lost -60% or -$120,000 from $200,000 leaves you with a balance of $80,000.

- Your average return is 20%, your real return is -20%

This hypothetical equation is how investors are sold on potential. The fact of the matter is, as an investor, it’s not how much you earn. It’s how much you keep that is important. If you never lose, you can be much farther along in the future.

- If you invest $100,000 and have a 100% gain in the first year, at the end of the year, your balance is $200,000.

- In year two, the market drops 60% and you lose nothing. At the end of the year, you have $200,000 and your average return is 50%.

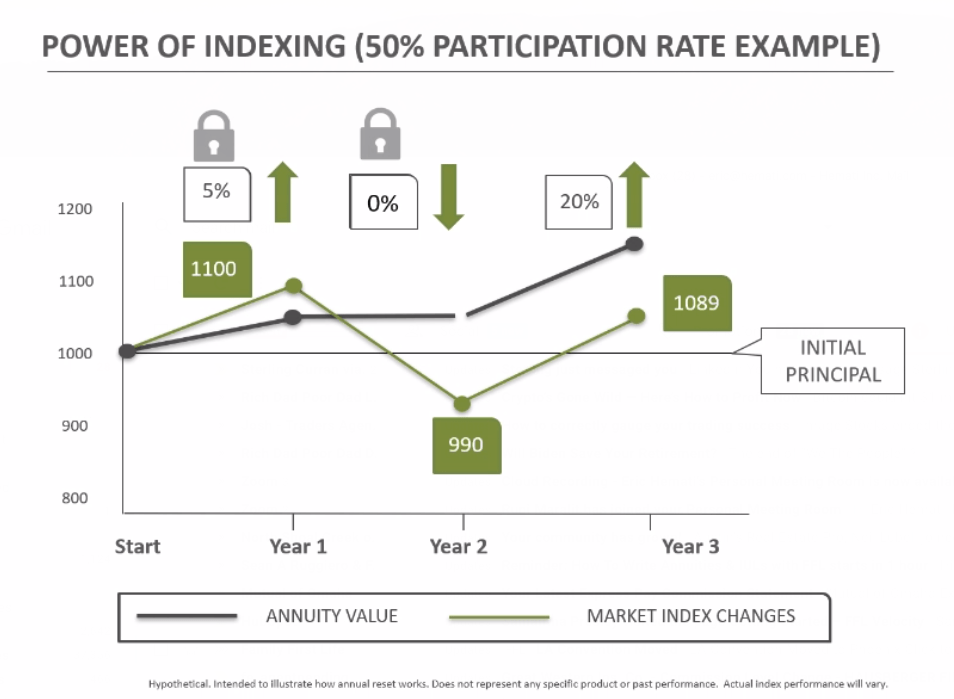

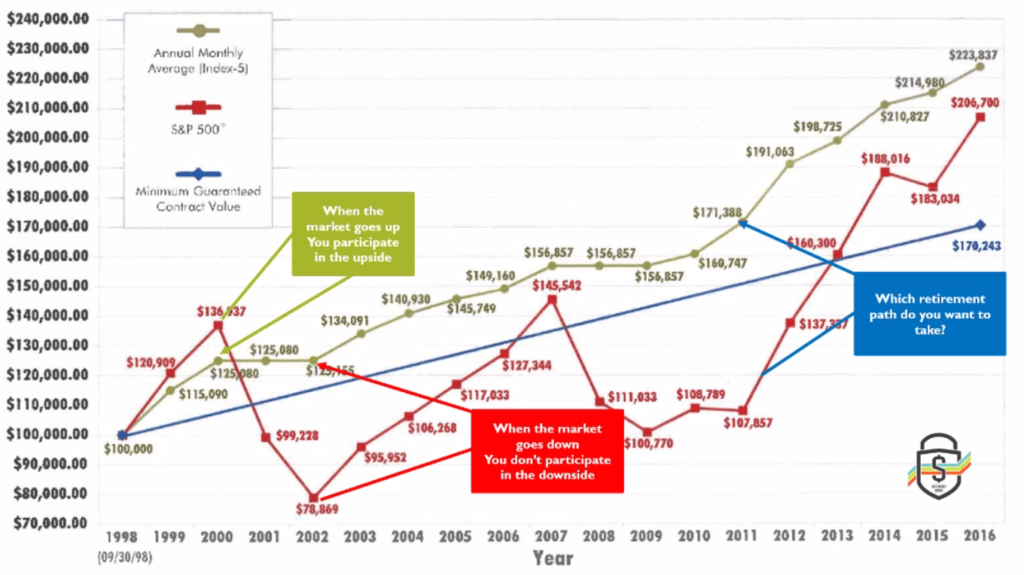

This is the power of indexing. Indexing is getting upside growth when the index is growing, and NEVER losing when the markets are falling. At each contract anniversary, you lock in the gains of the past year and reset for the next year, never turning back. This feature is referred to as annual reset.

When you have the power of indexing, coupled with a personal pension, you now have an equity index annuity. These two features, indexing and your “pension” (or income rider) provide two values on your contract.

Personal pension: To create your personal pension, add a lifetime income rider. Although different companies may call this rider by a variety of names, the insurance contract will guarantee a certain rate of return (currently 6%-7% compound interest at time of writing) until a time in the future, (which you choose) when you begin your “pension,” or payments to you for the rest of your life.

0 Comments